A note for QuickBooks ProAdvisors whose clients manage loan portfolios

Chances are you’ve seen this before. A client comes to you running a private lending fund, an agricultural co-op, or a small investment group. They’re managing their loan portfolio in QuickBooks because it’s what they know — and because no one ever told them there was something built specifically for what they do.

The problem surfaces slowly. Loan balances that don’t tie out. Amortization schedules living in a spreadsheet somewhere. Borrowers calling to ask questions the client can’t answer cleanly. And eventually, the reconciliation work lands on your desk.

QuickBooks is an excellent accounting tool. It was never designed to be a loan management platform.

What Breaks When Lenders Use QuickBooks Alone

There’s no native amortization engine. Clients build manual schedules in Excel, and those schedules break the moment a payment is late, a rate adjusts, or a loan gets modified mid-term. The downstream effect is interest accruals posted by hand, principal balances that drift from reality, and a quarter-end that turns into an untangling exercise.

There are no borrower statements. Clients either improvise something in Word, or they call you to explain why the numbers on their end don’t match what the borrower thinks they owe.

Loan-level portfolio reporting doesn’t exist without exporting data and rebuilding it in Excel — which means the numbers are already stale by the time anyone reads them.

Tracking fees, penalties, security deposits, and miscellaneous charges? Those get improvised too — usually as manual journal entries that nobody can explain six months later.

These aren’t edge cases. They’re the predictable result of using general-purpose accounting software to do a specialized job.

The Accounting Problem Underneath the Lending Problem

Even when a client maintains a passable amortization schedule in Excel, the accounting side is where things quietly fall apart.

In a properly structured loan portfolio, every transaction has a GL story. QuickBooks has no concept of how to tell it:

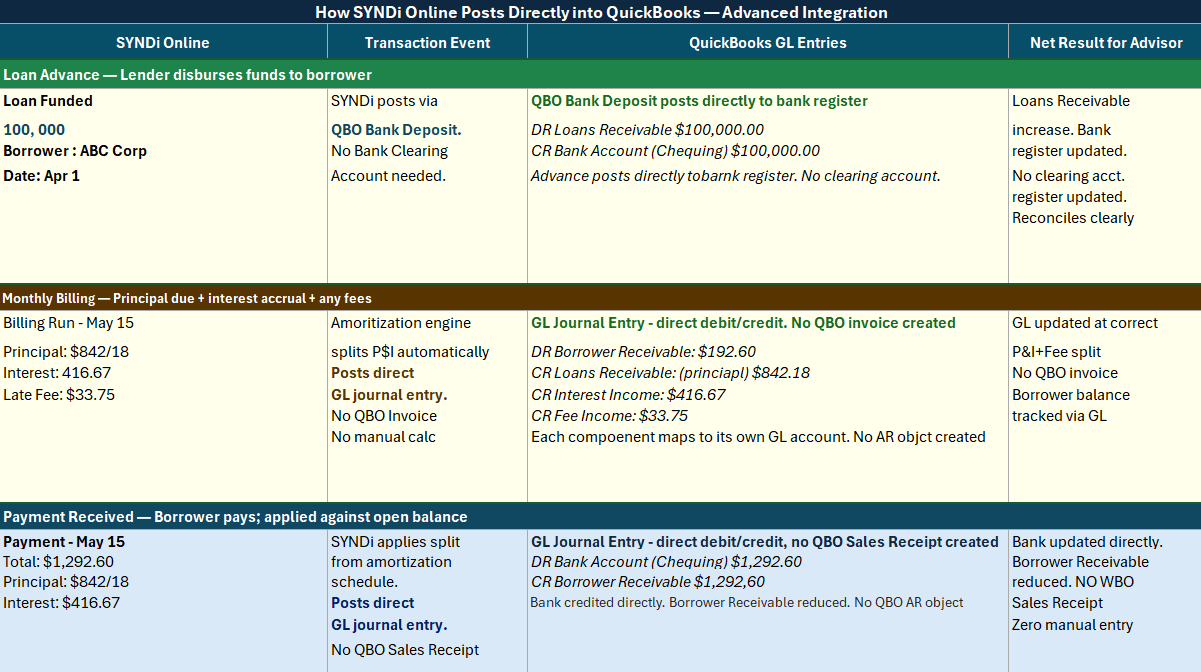

- Loan advance | Debit Loans Receivable, credit the bank. Straightforward — until the advance has to appear correctly in the bank register and someone has to figure out the timing.

- Monthly billing | That $1,292.60 invoice isn’t one number — it’s $842.18 of principal reduction, $416.67 of interest earned, and a $33.75 fee on top. Each piece hits a different account. Someone has to calculate that split every month, for every loan.

- Payment received | The split has to be applied correctly: reduce Borrower Receivables, credit the bank directly. If the payment was short or late, the math changes.

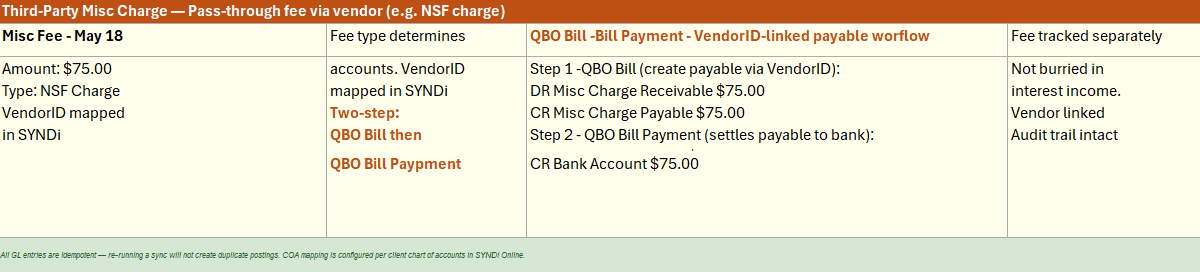

- Third-party fees | NSF charges, pass-through fees — these need their own payable workflow against a vendor, not buried in interest income or posted as miscellaneous deposits.

QuickBooks has no concept of this split. It doesn’t know what portion of a payment is principal, what’s interest, and what’s a fee. Someone has to calculate that manually and enter it. Every month. For every loan. And if the schedule was wrong, or a payment was short, or the rate changed — the entries are wrong too, silently, until reconciliation time.

The result is a receivables ledger that can’t be trusted. Interest income that’s either overstated or understated. An AR aging report that means nothing because the underlying entries weren’t structured correctly to begin with.

What We Built Instead

SYNDi Online is cloud-based loan management software built specifically for small lenders who’ve outgrown their current setup but don’t need enterprise-grade complexity.

It handles the full loan lifecycle in one platform: origination and funding, automated amortization, billing runs, payment processing, borrower statements, and real-time portfolio reporting. The amortization engine runs automatically — calculating principal and interest splits, handling variable rate adjustments, missed payments, partial payments, and mid-term modifications — without anyone touching a spreadsheet. Borrowers get statements on demand. Lenders get a live view of their entire portfolio: outstanding balances, arrears, upcoming maturities, yield analysis.

We’ve been building this for over 20 years, working with community lenders, agricultural co-ops, Indigenous financial institutions, dioceses, and private funds across Canada, the United States, and internationally.

How the GL Actually Works: SYNDi Online + QuickBooks

The integration doesn’t replace QuickBooks. It makes your clients better QuickBooks users. Every lending transaction is calculated correctly at the source — in SYNDi Online — and then posted to QuickBooks using our QuickBooks Integration built with Intuit’s QuickBooks REST API mapped to your clients’ own chart of accounts. Loan advances post as a QBO Bank Deposit directly to the bank register. Billings and payments post as direct GL journal entries — principal, interest, and fee splits calculated automatically, no manual entry required. Third-party misc charges route through a QBO Bill and Bill Payment via VendorID. No clearing account. No interim step to manage.

The diagram below shows exactly how each transaction type flows from SYNDi Online into the QuickBooks GL:

Figure 1: Integration GL flow. Loan advances post as a QBO Bank Deposit to the bank register. Billings and payments post as direct GL journal entries. Third-party misc charges route through a QBO Bill and Bill Payment via VendorID. All entries are idempotent and COA-mapped per client.

A few things worth noting for your clients’ books specifically:

- Direct bank posting | Loan advances post as a QBO Bank Deposit directly to the bank register — no intermediary clearing account, no extra reconciliation step. Payments post as direct GL journal entries: bank debited, Borrower Receivable credited.

- Direct GL posting for billings and payments | Billings and payments post as journal entries directly to the GL. No QBO Invoice or Sales Receipt is created. Borrower Receivable, Interest Income, Loans Receivable, and bank accounts update correctly without a QBO AR object.

- Idempotent posting | Re-running a GL transfer will not create duplicate entries. SYNDi Online keeps a record of each entry sent to QuickBooks, reassuring there are no duplicates sent.

- COA mapping | SYNDi Online mapped to your client’s chart of accounts drives everything. Loans Receivable, Interest Income, Fee Income — each loan is mapped to whatever account your client already uses in QuickBooks.

- Third-party fee workflow | Pass-through charges route through Misc Charge Payable with a VendorID, then settle via Bill Payment directly to the bank. Fees stay out of interest income and carry a clean audit trail.

For you as the ProAdvisor, this means the AR aging reconciles to the loan register. Interest income ties to what the amortization schedule says was earned. The balance sheet loan receivable balance matches the portfolio report. These are things that almost never happen cleanly when a lender is using QuickBooks alone.

Why This Matters for ProAdvisors

When a lending client runs SYNDi Online alongside QuickBooks, your work changes. You spend less time untangling manual accruals and explaining why balances don’t tie out, and more time on the advisory work that actually moves the needle for your clients.

We’re building a partner program specifically for ProAdvisors whose clients operate in lending or investment management:

- Referral commissions | Advisors who refer clients earn a commission on every conversion. No quotas, no complicated terms — if a client you refer becomes a SYNDi customer, you earn on it.

- Integration roadmap input | ProAdvisors who join the program now get direct input into the QuickBooks integration roadmap, so the tool gets shaped by people who understand how their clients’ books actually work.

- Natural advisory add-on | For clients who fit the profile, this becomes a complement to the work you’re already doing — not a competing product, a cleaner upstream data source.

The clients who fit this program are ones you likely already recognize: private lending funds tracking portfolios manually, ag co-ops managing repayment schedules, small investment groups issuing loans to members, or anyone who calls you because their loan balances don’t tie out.

If This Sounds Relevant

We’re not asking for a commitment. We’re asking for 15 minutes to walk through SYNDi Online and the partner program together. If your clients aren’t the right fit, no pressure. If they are, this becomes a natural complement to the advisory work you’re already doing — and a cleaner QuickBooks experience for everyone involved.

About SYNDi Group

SYNDi Group is a division of INDUSFLOW Systems Inc., based in Markham, Ontario. We have been developing purpose-built lending software for over 20 years, serving community lenders, agricultural co-operatives, Indigenous financial institutions, Catholic dioceses, and private investment funds across Canada, the United States, and internationally.